Rising Demand for Printed Circuit BoardsSignals Pakistan’s Expanding Tech Manufacturing Base

During the first half of 2025, Pakistan’s electronics sector has shown strong signs of growth, reflected in the rising imports of Printed Circuit Boards (PCB)

According to verified trade data from NBD DATA

This growth trend underscores Pakistan’s ongoing shift toward technology-based industrial production — particularly in electronics assembly, renewable energy systems, and small-scale automation equipment.

Import Dynamics: Consistent Monthly Growth Led by Early-Year Orders

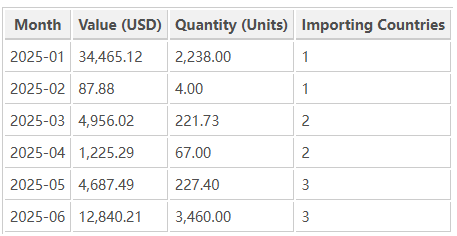

Data shows that PCB imports fluctuated moderately in the first quarter before accelerating toward mid-2025. The highest monthly import value was recorded in January 2025 at USD 34,465, followed by a secondary surge in June 2025, reaching USD 12,840 — more than double April’s level.

The surge in June aligns with an increase in PCB demand for local assembly projects in Lahore and Karachi’s industrial clusters, where small electronics manufacturers rely heavily on imported printed circuit boards for power modules, solar inverters, and consumer devices.

Leading Importers: A Concentrated Market of Small-Scale Electronics Firms

The NBD import database reveals that Pakistan’s PCB import market is dominated by a handful of specialized firms sourcing directly from East Asia and the Gulf.

Key importers during the period include:

ALAYA TRADING CO. — the largest importer, purchasing 951 units worth USD 21,009, primarily from Tucheng Good Trading Ltd.

AHMED ENTERPRISES — imported 521 units valued at USD 11,444, also from the same Taiwanese supplier.

DELUXE ELECTRIC STORE— focused on bulk imports of 3,300 PCBs, worth nearly USD 9,537, from Changsha J&W Electronics Corporation Ltd. in China.

MEDICAL DEVICES PVT. LTD. — imported 1,000 PCBs, worth USD 7,377, used in the assembly of healthcare-related diagnostic equipment.

MIAZ CORPORATIONS— a smaller-scale importer that procured 220 PCBs from Chen Xing Trade Co., Ltd., signaling active participation in low-volume electronics manufacturing.

These importers together account for nearly 85% of Pakistan’s total PCB import value during the first half of 2025, emphasizing the strong linkage between small-medium manufacturing enterprises and foreign suppliers.

Top Exporting Partners: China, UAE, and Taiwan Drive the Flow

Pakistan’s primary supply chain for PCBs continues to depend on three major trade hubs: China, Taiwan, and the United Arab Emirates.

-

China remains the most dominant exporter, with firms such as Weller Technology Co., Ltd., Changsha J&W Electronics Corporation, and Suzhou Rockcore Import & Export leading shipments.

-

Taiwan contributes through Tucheng Good Trading Ltd., providing specialized PCBs for power electronics and control circuits.

-

UAE acts as a re-export hub, facilitating logistics through Voltix Equipment Trading LLC and Bab Albahr Engineering Equipment LLC.

This supply network reveals how Pakistan sources both low-cost standard PCBs from China and mid-range customized components through Taiwanese intermediaries — a sign of an evolving electronics manufacturing ecosystem.

Market Interpretation: Growing Electronics Demand within Pakistan

The consistent monthly import of PCBs, though modest in value compared to global scales, reflects a structural trend in Pakistan’s economy:

-

Shift toward local assembly – many SMEs are assembling LED systems, power inverters, and IoT-related devices domestically.

-

Support for renewable energy – PCBs are essential components in solar charge controllers and inverter boards, particularly relevant as Pakistan’s renewable installations grow.

-

Emerging contract manufacturing – small firms are engaging in low-volume orders for regional electronics brands, signaling the birth of an electronics subcontracting market.

These developments mark an important step toward the formation of a diversified manufacturing base — one that gradually moves Pakistan beyond textile and leather exports into value-added technology production.

Case Insight: Alaya Trading and the Taiwan Connection

Among importers, ALAYA TRADING CO. provides an interesting case study.

Its transactions with Tucheng Good Trading Ltd. suggest the establishment of a steady supply pipeline for PCBs used in consumer electronics and renewable-energy devices. The repeated small-batch imports reflect a just-in-time model typical of developing manufacturing hubs, where firms avoid large inventories yet maintain constant production flow.

This dynamic mirrors patterns observed in Vietnam and India a decade earlier, when incremental PCB imports preceded the rise of domestic PCB assembly plants and electronics subcontracting networks.

Future Outlook: Toward Localization and Technical Upgrading

While Pakistan’s PCB import value remains relatively small, the composition of its importers shows growing diversification in end-use sectors — from industrial automation to medical and energy systems.

As domestic firms expand capacity, we can expect:

-

Greater demand for multilayer and high-precision PCBs, particularly for power conversion and automation.

-

Rising collaboration with Chinese and Taiwanese suppliers for joint assembly or technical training.

-

Policy incentives aimed at developing local PCB manufacturing, potentially under CPEC industrial zones or Special Economic Zones (SEZs).

If these developments continue, Pakistan could see its electronics manufacturing value chain mature significantly by 2027–2028, with domestic PCB production supplementing — rather than replacing — current import flows.

Conclusion

The steady import of Printed Circuit Boards (HS 85340000) during early 2025 confirms Pakistan’s growing appetite for electronics components.

With USD 58 thousand worth of PCBs imported within six months and strong participation from regional suppliers in China, Taiwan, and the UAE, the foundation for a more robust technology manufacturing base is clearly being laid.

This evolution represents not only a diversification of Pakistan’s industrial economy but also a significant step toward integrating into the global electronics supply chain.

Data Source

All data used in this report originates from the verified trade intelligence system of NBD DATA

, covering Pakistan’s import transactions between January 2025 and June 2025.

For in-depth datasets and analytical services, please visit https://en.nbd.ltd/service