Trade Review: Panama’s Growing Demand for Electrical Cables in Early 2025

In the first half of 2025, Panama’s imports of electrical cables showed renewed momentum, reflecting continued investments in infrastructure, industrial automation, and residential construction. According to NBD DATA

Total imports reached approximately 34,515 units, with an overall customs value of USD 70,758.66. This stable trade flow highlights Panama’s increasing reliance on advanced wiring systems to support public and private sector projects.

Imported products included a variety of cable types such as copper electrical cables, EPR and XLPE insulated power cables, and LAPP ÖLFLEX CLASSIC industrial cables, showing the country’s preference for durable, safety-certified electrical materials suitable for both power and signal transmission.

Monthly Trade Overview

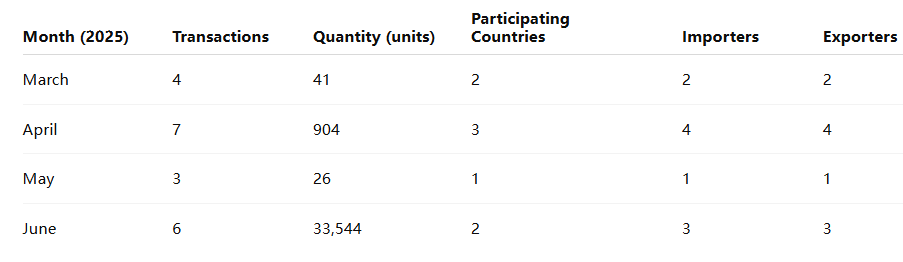

Panama’s imports of electrical cables under HS 854449900090

The dramatic increase in June 2025, when imports surpassed 33,000 units, represented more than 97% of total shipments for the period. This peak reflects multiple infrastructure and maintenance projects launched by both public agencies and private enterprises.

Major Importers and Suppliers

The Panamanian market remains relatively concentrated, with a handful of importers accounting for most of the trade volume.

Autoridad del Canal de Panamá (Panama Canal Authority) ranked as the largest importer, bringing in over 33,512 units of cables valued at USD 53,670, supplied by Hebei Huatong Wires and Cables Group Co., Ltd.

PETROAUTOS S.A. followed as a key importer, sourcing from MOBIS PARTS MIAMI, LLC.

Automatizaciones Industriales y Fluido imported specialized cables from LAPP PANAMA, S.A.

Additional active importers included:

Bombas y Balineras S.A.(supplier: Rotoline Equipamentos Industriais LTDA.

) -

Grupo Todo a Dólar S.A.(supplier: Great Buy Products

) La Casa del Embobinador S.A. (supplier: Tramar Industrial LTDA.

) Promoción Médica S.A. (supplier: Mettler Toledo, Thermo Fisher, Steris

)

Together, these firms represent the full scope of Panama’s cable import ecosystem — covering infrastructure, industrial, automotive, and consumer markets.

Exporting Countries and Product Origins

Panama’s electrical cable imports during this period originated mainly from China, Brazil, the United States, and Germany. Chinese producers such as Hebei Huatong supplied the bulk of industrial-grade cables for infrastructure projects. Brazilian company Rotoline provided heavy-duty equipment cables, while LAPP PANAMA represented Germany’s premium industrial cable segment.

This import mix indicates that Panama continues to rely on both Asia for volume and Europe for quality to meet diverse sectoral needs.

Product Range and Applications

Customs samples under HS 854449900090

-

Copper cables with EPR and XLPE insulation;

-

Industrial power and control cables;

-

Flexible ÖLFLEX CLASSIC cables;

-

Residential insulated wiring.

Market Trends and Industrial Outlook

Panama’s cable import trends in 2025 reflect:

-

Infrastructure-driven demand, led by Panama Canal modernization projects.

-

Expansion of industrial automation, with increasing adoption of control wiring.

-

Stable commercial consumption, particularly in retail and automotive applications.

Summary

Between January and June 2025, Panama imported over 34,000 units of electrical cables (HS 854449900090

Key buyers such asAutoridad del Canal de Panamá

Data Source

All figures and company information are derived from NBD DATA