Philippines’ Plastic Cup Imports Surge as Beverage and Retail Sectors Expand

According to data from NBD DATA

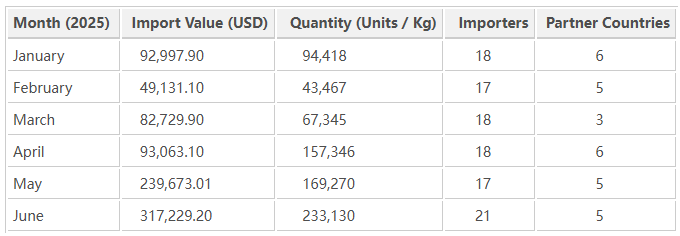

Between January and June 2025, total imports reached USD 874,824, equivalent to approximately 764.9 tons of plastic cups and related products. The country received 203 shipments from 8 partner nations, with imports handled by 69 companies and supplied by 85 exporters.

Representative import entries include popular consumer and commercial packaging items such as “MIXUE PLASTIC CUP (FROSTED),” “STARBUCKS CUP 16OZ COLD – MADE OF PLASTIC,” and “PLASTIC CUP WITH LID SIZE 12OZ–22OZ.” These show how the local café and retail drink industries are fueling demand for disposable and branded plastic containers.

Monthly Import Trend

Plastic cup imports into the Philippines maintained a modest yet consistent pace across the first six months of 2025, with peaks observed in May and June that aligned with higher beverage consumption and supply preparation for summer.

The data illustrate a clear upward trend from April through June, when imports surpassed USD 600,000 combined, reflecting both retail seasonality and expanded consumption of cold beverages. These months coincided with the Philippines’ warm-weather peak, when café and convenience store sales traditionally surge.

Market Observation: Leading Brands and Importers

The composition of imported goods reveals the growing role of international beverage chains, local cafés, and packaging distributors in shaping the plastic cup market.

-

Mixue and Shell Café branded frosted cups dominate the mid-range product line, catering to popular tea and coffee chains across Metro Manila and provincial cities.

-

Starbucks imports a series of cold plastic cups (12oz–20oz Tritan models), reflecting the company’s ongoing sustainability shift toward reusable and recyclable materials.

-

MR.DIY, Langma, and Whey King feature in household and fitness product imports, showing diverse applications for plastic cups in everyday retail and sports accessories.

The market remains highly competitive, with suppliers from China, Vietnam, and Malaysia serving as key exporters, providing both OEM products and branded packaging for Philippine food and beverage businesses.

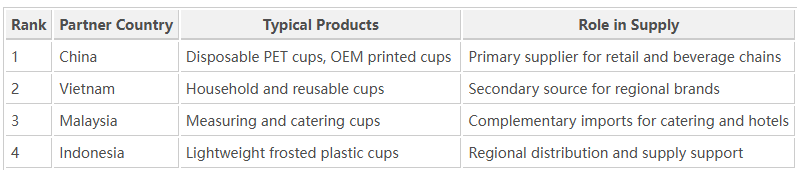

Trade Regions: China Dominates Supply

Trade analysis shows that China continues to be the leading supplier of plastic cups to the Philippines, delivering cost-efficient disposable and PET-based cup models. Chinese manufacturers provide a wide range of products — from custom-printed beverage cups to measuring and catering cups — meeting the demands of café chains and event service providers.

Other regional suppliers include Vietnam, Malaysia, and Indonesia, which collectively strengthen the supply chain for packaging goods within Southeast Asia.

Sectoral Demand and Industrial Drivers

The expansion of food packaging, convenience retail, and café culture is the main engine behind the rising import of plastic cups. The Philippines’ milk tea and coffee chain boom, led by brands like Mixue, Gong Cha, and Starbucks, continues to influence packaging trends.

Additionally, the country’s growing food delivery industry under GrabFood, Foodpanda, and other platforms fuels steady consumption of disposable containers and beverage packaging. This structural change in consumer behavior — toward on-the-go and takeaway consumption — has established plastic cups as a key import commodity for packaging firms and retailers alike.

Environmental considerations have also begun shaping import patterns. A number of Philippine distributors now source BPA-free and Tritan plastic cups designed for recyclability, reflecting evolving regulations and consumer awareness.

Summary

During January–June 2025, the Philippines imported nearly USD 875,000 worth of plastic cups, reflecting a healthy and expanding packaging market supported by beverage retail and quick-service food industries.

The rise of branded cup imports, led by Mixue and Starbucks, along with China’s continued dominance in supply, highlights the Philippines’ dependence on regional trade networks for packaging materials.

With the steady growth of café chains, food delivery services, and retail modernization, imports of disposable and eco-friendly plastic cups are expected to continue increasing in the second half of 2025.

Data Source

All trade data and company information cited in this article are derived from NBD DATA, based on the Philippines’ import statistics for HS 39241099000 (Plastic Cups) during January–June 2025.

For customized trade analysis and market insights, please visit https://en.nbd.ltd/service

.