Kenya’s Oil and Fuel Filter Imports Hit USD 6.79 Million in First Half of 2025

In the first half of 2025, Kenya’s imports of oil and fuel filters (HS code 84212300

Monthly Trends

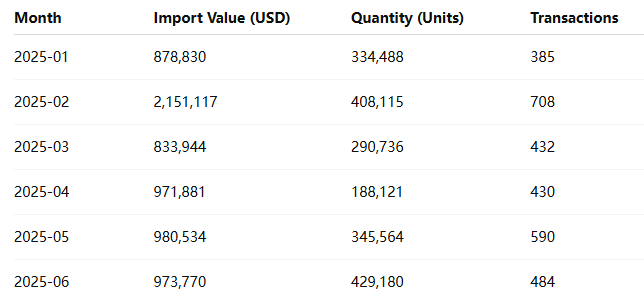

Kenya’s imports fluctuated slightly across the first half of the year but maintained a strong overall performance. The highest monthly import value was observed in February 2025, reaching USD 2.15 million, followed by steady inflows through May and June.

The data shows Kenya’s imports peaked early in the year, particularly in February, driven by pre-harvest season demand for agricultural machinery parts and replenishment of inventory by car service and parts distributors.

Market Overview

During January–June 2025, Kenya imported oil and fuel filters from 47 countries, engaging 468 importers and 699 exporters worldwide. This reflects an increasingly diversified supply chain and Kenya’s ongoing automotive industry growth.

Leading supplier nations included China, India, and Germany, which collectively accounted for over half of the import value. These countries dominate the production of oil and fuel filters used in commercial trucks, passenger vehicles, and construction equipment.

Product descriptions sampled from import data indicate a wide range of items such as engine oil filters, fuel filter cartridges, hydraulic filters, air/oil separators, and maintenance kits. Examples include:

-

“Caterpillar fuel/water separator filters”

-

“John Deere oil filter RE504836”

-

“Hengst oil filter (E500 KP02 D36)”

-

“Toyota genuine fuel filter assembly”

These products are typically used in the maintenance of engines for automobiles, tractors, and industrial generators — highlighting Kenya’s increasing reliance on imported components to sustain its fleet of imported machinery.

Top Kenyan Importers

According to NBD DATA, the top Kenyan importers of oil and fuel filters during this period were:

Automotive Distributors Africa Ltd – A leading distributor handling multiple brands of oil and fuel filters, including Caterpillar and John Deere products.

AMK International – Specialized in wholesale importation of automotive spare parts, particularly oil filters and engine components from China.

Star Cargo Worldwide Ltd – Focused on logistics and bulk imports of automotive filters for both retail and OEM markets.

ICS Agri Ltd – Supplies agricultural and industrial filters, including engine oil filters for tractors and farm equipment.

Auto Parts Warehouse Kenya – A mid-sized importer catering to local garages and independent mechanics.

These companies form the core of Kenya’s filter supply chain, ensuring consistent availability of maintenance parts across the automotive and industrial sectors.

Leading Supplier Companies

Kenya’s main external suppliers were diverse but primarily concentrated in Asia and Europe. Among the most active exporters were:

Hengst Filters (Germany) – A globally recognized producer of premium automotive filters for both passenger and heavy-duty vehicles.

Ashok Leyland Ltd (India) – Exported specialized diesel engine filters, including water separators and fine fuel filtration systems.

Guangzhou Hangsheng Auto Parts Co., Ltd. (China) – Provided low-cost oil and fuel filters under private labels for regional distributors.

Atlas Copco (Sweden) – Supplied industrial compressor oil separators and maintenance kits.

John Deere (U.S.) – Exported agricultural and industrial engine filters for Kenyan distributors.

Together, these firms reflect Kenya’s wide import spectrum, ranging from low-cost aftermarket filters to OEM-grade components for high-end machinery.

Trade Regions

In the first half of 2025, Kenya sourced filters from 47 countries, but imports were highly concentrated among top regions:

-

Asia (China, India, South Korea, Japan) – ~60% of total imports

-

Europe (Germany, UK, Sweden, Italy) – ~25%

-

North America (USA) – ~10%

-

Other regions (UAE, South Africa, Turkey) – ~5%

This diversification ensures supply resilience, as Kenya benefits from competitive pricing in Asia and technical quality from Europe and the U.S.

China and India remain the cornerstone suppliers due to their strong export capabilities for aftermarket filters and components used in Kenya’s imported vehicle fleet — mostly second-hand Japanese and European cars.

Market Observation

Kenya’s demand for oil and fuel filters has expanded in parallel with the growth of its used-car market and industrial sectors. Importers have increasingly diversified sourcing to balance cost and quality — a trend evident in the rise of mid-tier brands like Hengst, Teson, and Klik Autotech alongside premium suppliers like John Deere and Caterpillar.

The agricultural machinery segment also contributed significantly to this growth, with filters imported for tractors, harvesters, and irrigation engines, particularly from India and China.

As the country continues to modernize its logistics and construction industries, the need for reliable filter systems — critical for reducing engine wear and improving efficiency — is expected to grow steadily.

Regional Focus: China

China remains Kenya’s largest single supplier of oil and fuel filters in both quantity and value. Chinese manufacturers such as Guangzhou Hangsheng and Jingling Auto Parts have captured a dominant share through affordable pricing and broad product compatibility.

Typical imported Chinese products include:

-

“Oil Filter for Toyota/Isuzu Models”

-

“Fuel Filter Element Assembly”

-

“Hydraulic Oil Separator”

These products are widely used in Kenya’s automobile servicing network, particularly by small and medium-sized workshops that rely on cost-effective parts.

Conclusion

Between January and June 2025, Kenya’s imports of oil and fuel filters (HS 84212300) totaled USD 6.79 million, with more than 1.99 million units imported from 47 countries. The market is dominated by suppliers from China and India, supported by European OEM brands offering high-end solutions.

This sustained import activity underlines Kenya’s expanding automotive maintenance industry and its crucial dependence on global suppliers for essential components. As vehicle ownership, agricultural mechanization, and industrial activity continue to grow, demand for filters is projected to remain robust in the second half of 2025.

Data source: Official import records analyzed by NBD DATA. For detailed trade tracking or supplier verification services, please visit https://en.nbd.ltd/service.