Indonesia’s Fresh Mangosteen Exports Exceed USD 16.35 Million in Late 2024

Indonesia consolidated its global leadership in the tropical fruit trade during the second half of 2024, as fresh mangosteen (HS 08045030) exports reached a total value of USD 16.36 million.

According to NBD DATA

The remarkable performance underscores Indonesia’s growing dominance in premium tropical fruit markets across Asia and beyond.

Export Overview

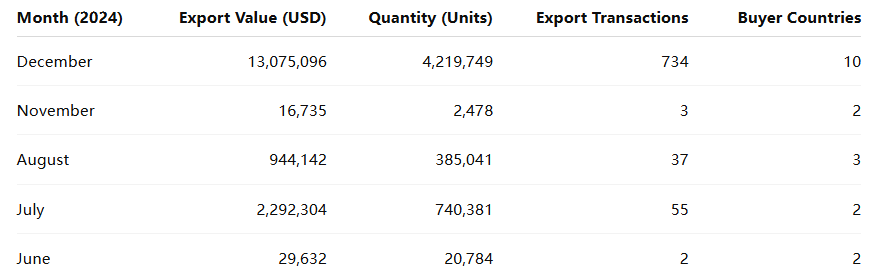

Between June 30 and December 31, 2024, Indonesia’s fresh mangosteen exports recorded strong and consistent growth.

The trade flow involved 47 exporters and 50 international buyers, reflecting an increasingly diversified global supply chain.

The export surge peaked in December 2024, when mangosteen shipments accounted for roughly 80% of total half-year export value, confirming Indonesia’s ability to align production cycles with international demand periods—particularly the East Asian winter season.

Key Importing Markets

During the reporting period, Indonesian mangosteens reached ten countries, with the People’s Republic of China standing out as the largest buyer, followed by Singapore, Malaysia, and Vietnam.

These countries collectively accounted for more than 95% of total export value.

Market Highlights

-

China: The leading destination, driven by premium retail demand in major cities such as Shanghai, Guangzhou, and Beijing.

-

Singapore: A strategic re-export and testing hub for ASEAN fruit logistics.

-

Malaysia & Vietnam: Stable regional buyers, maintaining year-round demand for mangosteen as a luxury fruit.

-

United Arab Emirates: Emerging as a small but steady market via re-export channels to the Middle East.

The dominance of Asian markets reflects Indonesia’s logistical advantage and the freshness requirement of mangosteen exports, which favor short transit times and efficient cold-chain handling.

Top Buyers

Trade data from NBD DATA

The top buyers by trade value include:

-

BEIJING JUNYAO INTERNATIONAL

— USD 5,605,777 -

BEIJING JUNHUI INTERNATIONAL TRADING CO., LTD. — USD 2,765,971

-

SHANGHAI SUNSHINE AGRICULTURE TECHNOLOGY CO., LTD. — USD 1,048,746

-

CHUANNONGJING (HAINAN) INTERNATIONAL TRADE CO., LTD. — USD 388,773

-

CHUN WAN YI (GUANGZHOU) SUPPLY CHAIN MANAGEMENT CO., LTD.

— USD 594,194

Together, these companies accounted for nearly 65% of Indonesia’s total mangosteen export value, highlighting the strong dependence on Chinese wholesale and retail markets.

Chinese buyers often act as import distributors, channeling fresh mangosteen to multiple provinces for online and offline fruit markets.

Leading Indonesian Exporters

Indonesia’s export structure is characterized by a vibrant mix of large-scale agricultural firms and smaller fruit consolidators.

Top exporters include:

-

PT. ANUGERAH UTAMA PUSPA INDONESIA

— active in multiple buyer partnerships -

PT. BUMI INDO NUSANTARA ABADI — large-volume supplier to Shanghai and Beijing

-

PT. GHF AGRO MANDIRI — high consistency in delivery and quality

-

CV. PUTRI CIKAL MUSTIKA SEJATI

— specialized in export packaging -

PT. MAHKOTA MANGGIS SEHATI — emerging mid-sized exporter

These companies together managed a significant share of the December export boom, with PT. BUMI INDO NUSANTARA ABADI alone handling over 300,000 units in that month.

Seasonal and Production Factors

Indonesia’s mangosteen production follows a distinct seasonal cycle, with peak harvests occurring between October and February.

This natural timing aligns perfectly with export demand from northern Asia, where tropical fruit consumption rises during the winter months.

Key Production Areas

-

West Java (Tasikmalaya, Subang, Purwakarta): Known for premium-grade mangosteen with uniform size and high sweetness.

-

Bali & Lombok: Supply niche export varieties with superior aesthetic quality.

-

Sumatra (Lampung & North Sumatra): Emerging production zones with growing export capacity.

Improved post-harvest handling and cold-chain infrastructure—supported by Indonesia’s Ministry of Agriculture—have been crucial to maintaining fruit quality during long-distance shipments.

Export Supply Chain and Logistics

The mangosteen export process typically involves multiple specialized stages:

-

Collection and Sorting: Exporters consolidate fruit from local cooperatives and farmers, grading by size and color.

-

Packaging: Use of ventilated cartons or mesh bags designed to prevent bruising and heat accumulation.

-

Pre-cooling and Quality Control: Warehouses near Jakarta and Surabaya serve as key pre-export centers.

-

Air Freight: Given the fruit’s sensitivity, most high-value shipments are exported via air, especially to China and Singapore.

This cold-chain discipline enables Indonesia to deliver mangosteens at peak freshness—often reaching retail shelves in under 48 hours after harvest.

Price and Value Trends

The average unit export price for Indonesian mangosteen during H2 2024 was approximately USD 3.05 per kilogram equivalent, with noticeable variation across markets.

-

China: Premium-grade fruits achieved up to USD 3.40/kg.

-

Singapore: Averaged around USD 2.90/kg, reflecting its re-export function.

-

Malaysia and Vietnam: Generally lower, around USD 2.50/kg, for bulk shipments.

This pricing range reflects strong international positioning of Indonesian mangosteen as a mid- to high-value tropical fruit, competing favorably with Thai and Vietnamese exports.

Competitive Landscape

Indonesia’s rapid growth in mangosteen exports is reshaping regional competition:

-

Thailand, traditionally the world’s leading exporter, faced temporary declines in late 2024 due to adverse weather.

-

Vietnam maintained steady export volumes but with smaller fruit size and limited premium-grade supply.

-

Malaysia focused mainly on domestic consumption, leaving export markets largely to Indonesia and Thailand.

Indonesia’s ability to offer consistent quality, rapid logistics, and competitive prices has earned it preferred-supplier status in Chinese and Singaporean wholesale markets.

Trade Relationship Dynamics

The export data reveal recurring partnerships between specific Indonesian exporters and Chinese buyers, suggesting stable long-term contracts.

For example:

-

PT. BUMI INDO NUSANTARA ABADI consistently supplied both BEIJING JUNYAO INTERNATIONAL and SHANGHAI SUNSHINE AGRICULTURE TECHNOLOGY CO., LTD.

-

PT. ANUGERAH UTAMA PUSPA INDONESIA

served multiple importers including BEIJING GRIT TECHNOLOGY and SHANGHAI HOLDFRESH TRADING. -

PT. GHF AGRO MANDIRI diversified exports to three Chinese provinces through agents.

Such relationships underline the strategic maturity of Indonesia’s fruit export sector, which increasingly operates on contractual and branded supply chains rather than sporadic spot trading.

Regional Economic Impact

The surge in mangosteen exports has yielded tangible benefits for Indonesia’s local economies:

-

Farm-level earnings: Farmers in Java and Bali reported improved incomes from direct export-grade purchases.

-

Employment growth: Sorting, packaging, and quality control facilities expanded their seasonal workforce.

-

SME participation: More small- and medium-sized enterprises entered the export supply chain through subcontracting.

In addition, government-supported programs for fruit traceability and Good Agricultural Practices (GAP) certification have enhanced international confidence in Indonesian produce.

Challenges and Quality Standards

Despite the strong export performance, several operational challenges persist:

-

Pest and phytosanitary compliance: Exporters must meet stringent requirements for pesticide residue and pest control, especially for China and Japan.

-

Cold-chain limitations: Some secondary production regions lack consistent refrigeration infrastructure.

-

Market concentration: Heavy dependence on China increases vulnerability to demand shifts or import restrictions.

To mitigate these issues, exporters are investing in packhouse upgrades, traceability systems, and partnerships with logistics providers to maintain export readiness throughout the season.

Sustainability and Future Potential

The expansion of mangosteen exports also raises questions about long-term sustainability.

Government agencies and private associations are now emphasizing eco-friendly cultivation, reduced pesticide use, and training programs for farmers to ensure the sector’s continued growth.

The Ministry of Agriculture’s 2025 agenda includes:

-

Developing certified organic mangosteen clusters.

-

Expanding export access to Japan and South Korea.

-

Promoting geographical indication labeling for premium mangosteen from specific regions like Subang or Tasikmalaya.

These initiatives aim to sustain Indonesia’s export growth while positioning mangosteen as a signature tropical fruit with global brand recognition.

Outlook for 2025

The export outlook for 2025 remains highly positive. Key projections include:

-

Increased export value expected to surpass USD 20 million if favorable weather and logistics persist.

-

Expanded air-cargo capacity to China and Singapore during peak harvest months.

-

Higher adoption of quality certification to meet Japan and South Korea’s import standards.

With a growing base of experienced exporters and strong demand from Asian markets, Indonesia’s fresh mangosteen industry is poised to strengthen its global presence.

Conclusion

Indonesia’s export performance for fresh mangosteen (HS 08045030) during June–December 2024 illustrates the country’s ascent as a tropical fruit powerhouse.

With exports surpassing USD 16.35 million and over 5.36 million units shipped, Indonesia confirmed its role as one of Asia’s premier suppliers of premium mangosteen.

Strong partnerships with Chinese importers, improved logistics, and expanding smallholder participation have positioned the country for continued success in 2025 and beyond.

As global consumers increasingly value freshness and quality, Indonesia’s mangosteen industry is set to remain at the forefront of the international tropical fruit trade.

Data Source

All figures in this article are derived from verified trade statistics by NBD DATA

For tailored export intelligence and market analysis, please visit NBD DATA Services