From Lock&Lock to Miniso: China Leads Indonesia’s Water Bottle Supply Chain

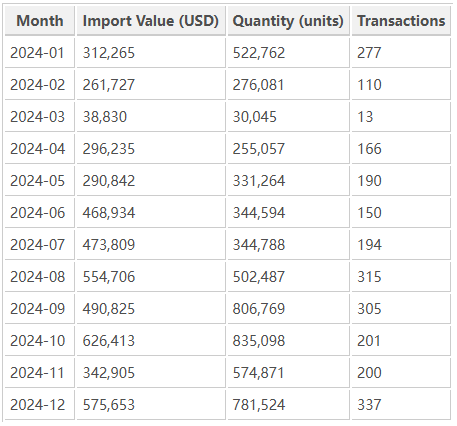

In 2024, Indonesia’s imports of WATER BOTTLE under HS Code 39241099 showed remarkable growth, reflecting the nation’s expanding retail and consumer goods sectors. According to data from NBD DATA, the total import value reached USD 4.73 million, with a cumulative 2,458 transactions and total imports exceeding 5.6 million units. Major product examples include popular consumer categories such as plastic sports water bottles and insulated portable bottles—trending consumer items often marketed by lifestyle brands in Southeast Asia.

Monthly Import Trends

The monthly data illustrate a clear upward trend throughout 2024. Imports peaked in December 2024, with a value of USD 575 thousand and more than 780,000 units, representing the year’s highest trade activity. Early in the year, volumes were relatively low—January’s total stood at 520,000 units—but subsequent months saw steady gains driven by strong retail and brand inventory cycles.

Overall, Indonesia’s import value for plastic water bottles increased steadily from mid-2024, aligned with retail restocking periods and consumer promotions in the fourth quarter. The diversity of supplier regions and product types points to a competitive yet China-dominated supply chain.

Market Overview

Indonesia imported water bottles from 9 partner countries in 2024, involving 156 importers and 187 exporters. Among the top importers were leading consumer goods companies and retail chains that leverage design, branding, and distribution to reach middle-class consumers. The strong retail link with Chinese suppliers highlights how global lifestyle trends are influencing Indonesian consumption.

Top Importers

The top Indonesian importers include:

PT. LOCK & LOCK INDONESIA— the largest importer, mainly from China’s Lock & Lock Vina and Samsung SDS China.

PT. DUTA INTIGUNA YASA — sourcing products from Guangzhou and Zhejiang suppliers specializing in household plastics.

PT. MINISO LIFESTYLE TRADING INDONESIA — in branded bottles under the Miniso franchise network.

PT. PASIFIK DISTRIBUSI INDONESIA — imports through Guangdong Blue Origin Supply Chain Technology Co., Ltd.

PT. DISTRIBUSI MEBEL NUSANTARA — smaller in value but part of IKEA Supply (Malaysia)’s extended logistics ecosystem.

These buyers show that Indonesia’s import landscape combines international retail brands, domestic distributors, and lifestyle product networks serving both mass and premium consumers.

Leading Suppliers

Chinese exporters overwhelmingly dominate Indonesia’s water bottle imports. The top suppliers include:

LOCK & LOCK VINA CO., LTD. — supporting Lock & Lock’s regional operations.

MINISO INTERNATIONAL GUANGZHOU LIMITED — supplying Miniso retail lines.

NINGBO AMBITION INTERNATIONAL TRADING CO., LTD.— specializing in OEM household plastics.

GUANGDONG BLUE ORIGIN SUPPLY CHAIN TECHNOLOGY CO., LTD. — operating as a key integrated trading hub.

ZHEJIANG SELIYA PLASTIC CO., LTD. — supplying molded plastic bottles to Indonesian distributors.

This structure demonstrates China’s comprehensive manufacturing capacity—from brand-specific OEM to low-cost contract production—supporting Indonesia’s rapidly expanding consumer goods sector.

Trade Regions

Indonesia’s import network for water bottles in 2024 primarily connected to East Asia. China remained the main source, with other smaller partners including Vietnam and Malaysia. This concentration underlines Indonesia’s reliance on Asian supply chains for cost-effective household plastics. The focus on CHINA reflects strong intra-Asia trade integration, with typical product examples such as Lock & Lock plastic bottles and Miniso portable flasks being repeatedly identified in customs records.

Market Observation

A deeper examination of the top trading companies reveals how retail brands and supply-chain integrators collaborate. Lock & Lock Vina Co., Ltd. operates as a regional export center, while PT Lock & Lock Indonesia handles distribution and retail channels nationwide. Miniso’s imports demonstrate how design-driven consumer goods reach mass markets efficiently via integrated logistics. Meanwhile, Guangdong Blue Origin Supply Chain illustrates how trading houses facilitate customized product development and flexible order cycles for Indonesian distributors.

This synergy between manufacturing in China and distribution in Indonesia underscores a key trend: the regionalization of the consumer-goods supply chain in Southeast Asia. The growing middle-income segment in Indonesia is driving steady demand for reusable water bottles—both as lifestyle products and as part of the broader sustainability shift.

Summary

Throughout 2024, Indonesia’s imports of plastic water bottles expanded in value and quantity. Monthly performance trends confirm solid momentum in the second half of the year, peaking in December. The market remains largely dependent on Chinese suppliers, which account for the majority of exports through key players like Lock & Lock Vina, Miniso International, and Guangdong Blue Origin Supply Chain Technology.

The data from NBD DATA suggest that Indonesia’s household-product imports will continue to rise, driven by lifestyle branding, retail expansion, and growing sustainability awareness among urban consumers.

Data Source

All trade data and company information in this report are provided by NBD DATA, based on 2024 import records for HS 39241099 (water bottles). For data subscription and enterprise analytics services, please visit our service page.