Smart Locks, Digital Security, and Hardware Growth: Inside India’s Lock Import Trends

According to NBD DATA

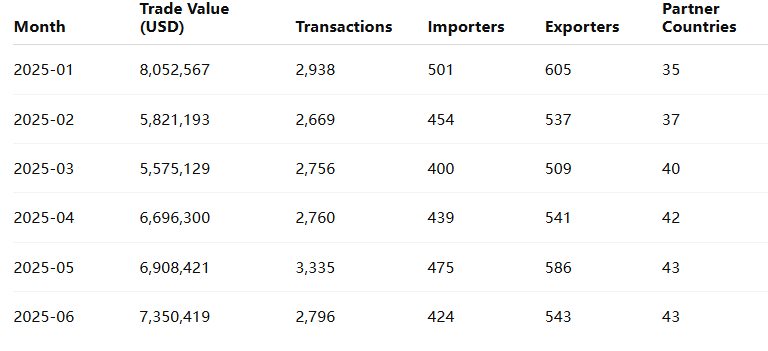

During this six-month period, India recorded 17,254 transactions, involving 1,316 importers, 1,682 exporters, and trade links with 55 countries.

Products under this category include electronic locks, hotel smart locks, combination padlocks, industrial latch systems, and digital security access devices, such as Yale Zuri Smart Lock, Anchor 7000 series, and RFM 712 ANSI electronic locks.

For technical specifications, see HS 83014090

Monthly Import Dynamics

India’s lock import performance in the first half of 2025 reveals consistent growth, reflecting rising demand in residential, commercial, and smart infrastructure sectors.

India’s import value remained steady from March onward, peaking at USD 7.35 million in June 2025, a 32% increase from January. This pattern highlights growing investment in digital locks for smart homes and industrial-grade latch systems used in machinery and construction.

Market Overview: Key Importers and Their Roles

India’s lock import ecosystem is led by both traditional hardware companies and smart technology integrators. The top importers collectively account for over 70% of total trade value.

-

NCR Corporation India Private Limited

— The largest importer with more than USD 6.39 million in imports. NCR sources locking systems and secure access components from DormaKaba USA Inc., Sargent & Greenleaf Inc., and Fujitsu Frontech Ltd., primarily for ATMs and secure cash handling systems. -

DormaKaba India Private Limited

— Imported USD 1.27 million, representing a significant share in high-end architectural hardware and hotel smart locks. Major suppliers include DormaKaba Deutschland GmbH, Kaba Ltd., and Beijing Ares-Lock Industry Co., Ltd. -

Kinlong Hardware India Private Limited

— A leading importer of USD 688,877, specializing in door and façade hardware. Its imports mainly come from Guangdong Kin Long Hardware Products Co., Ltd. in China, reflecting strong India–China supply integration in architectural fittings. -

Southco (India) Private Limited

— Imported USD 327,692, focusing on precision latches, compression locks, and industrial locking components used in vehicles, aircraft, and enclosures. -

Samsonite South Asia Private Limited

— With USD 790,612 in imports, Samsonite’s trade consists mostly of padlocks, smart luggage locks, and combination locking devices, mainly from Xian Kombo Import and Export Co., Ltd. and Jing Yu Lock (Hong Kong) Co., Ltd.

Together, these firms demonstrate India’s dual-market structure: a balance between architectural and industrial locking systems on one side and consumer-oriented smart and luggage locks on the other.

Regional Trade Landscape

India’s imports of HS 83014090 locks are globally diversified, with key origins including China, Germany, Switzerland, Hong Kong, and Singapore.

China remains India’s top supplier, providing both mechanical padlocks and advanced electronic locks. Notably, imports from Europe are concentrated in high-end digital systems — DormaKaba, Schneider Electric, and Southco products dominate commercial infrastructure projects.

The following trends define India’s regional import structure:

-

China — Core supplier of consumer-grade locks, smart locks, and industrial latch parts.

-

Germany & Switzerland — Suppliers of electronic access systems and premium building hardware.

-

United States — Key origin for secure electronic locks for ATMs and industrial use.

-

Singapore & Hong Kong — Regional hubs for re-exported smart locks and hotel locking systems.

This diversification helps Indian distributors stabilize supply and adopt new security technologies faster.

Emerging Technologies: From Padlocks to Smart Access

Recent import data highlights a transition toward digital and electronic locks, signaling India’s move toward intelligent building infrastructure.

Key product examples include:

-

Smart locks (Yale Zuri Smart Lock, Anchor A-7000, RFM 712 series)

-

Electronic combination locks for hotels and offices

-

Industrial compression latches and torque hinges (Southco, Mecha Locks)

-

ATM and equipment security locks (Sargent & Greenleaf)

-

Smart luggage locks integrated into Samsonite’s travel products

These innovations support India’s “Digital India” initiative, where physical security merges with connected technologies in homes, hotels, and transport systems.

Industry Insight and Forecast

The lock import sector in India mirrors the country’s infrastructure and digitalization trends:

-

Rising urbanization — Boosts demand for architectural hardware and access control systems.

-

Smart city projects — Drive adoption of digital and biometric locks.

-

E-commerce and logistics — Encourage imports of portable and TSA-compliant padlocks.

-

Industrial automation — Sustains demand for precision latches and safety locks in manufacturing.

Between 2025 and 2026, the segment is expected to grow by 8–10% annually, with smart and electronic locks leading the surge. Collaborations between Chinese, European, and Indian manufacturers will likely deepen, promoting local assembly and R&D in IoT-enabled locking systems.

Summary

India’s imports of locks (HS 83014090) reached USD 40.4 million from January to June 2025, supported by 1,316 importers and 1,682 exporters across 55 trade partners.

The market is dominated by firms like NCR, DormaKaba, Kinlong, Southco, and Samsonite, bridging consumer hardware with industrial applications.

The ongoing shift toward smart security systems and digitized access control positions India as one of Asia’s fastest-growing markets for locking technologies.

Data Source

All trade figures are sourced from NBD DATA

For detailed enterprise-level reports and dashboard services, visit NBD DATA Services