Top Importers and Suppliers in Mexico’s Growing Electric Cable Trade

In the first half of 2025, Mexico’s import market for electric cables (HS Code85444299

Notably, products such as power wiring harnesses and automotive electric cables dominated import categories, underscoring the vital role of electric cabling in supporting Mexico’s electronics, automotive, and infrastructure industries.

Monthly Trade Overview

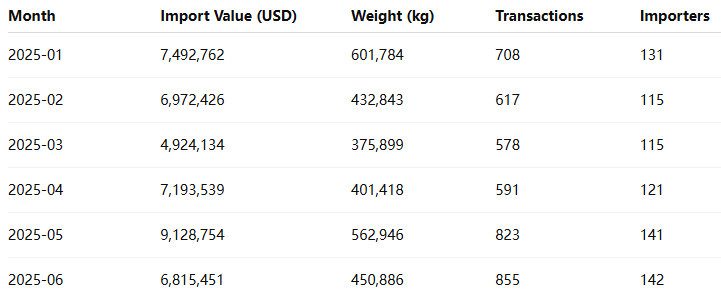

Monthly data illustrates a dynamic import flow throughout the six-month period. The market reached its highest import value in May 2025, amounting to USD 9.13 million, followed by a slight contraction in June. The first quarter remained relatively stable, averaging USD 6–7 million per month.

Throughout this period, import activity increased by roughly 30% between February and May, suggesting an expansion in industrial demand—particularly from automotive assembly and consumer electronics manufacturers. The surge in May can be attributed to intensified sourcing from East Asian partners.

Market Observation: Top Importers

Among the 355 active importers, several major companies led Mexico’s CABLE ELECTRICO imports, with notable participation from global manufacturing giants and local industrial players. The top importers, all verified by trade records, are as follows:

-

FOXCONN BAJA CALIFORNIA S.A. DE C.V.

– The largest importer in this category, with imports exceeding USD 3.48 million and over 358,000 units, largely for assembly of consumer electronics and wiring harnesses. -

HISENSE ELECTRONICA MEXICO S.A. DE C.V.

– Imported over USD 3.75 million, primarily serving its appliance manufacturing division in Nuevo León. ENSAMBLADORA VENTURA DE MEXICO S.A. DE C.V.– Specialized in automotive wiring components, importing around USD 2.11 million worth of cables.

IDL INTERNATIONAL DISTRIBUTION & LOGISTICS, S.A. DE C.V. – Recorded USD 2.86 million in imports, acting as a major logistics intermediary for Asian suppliers.

SCHNEIDER ELECTRIC MEXICO S.A. DE C.V. – Imported USD 0.33 million, focusing on high-voltage industrial cables and control systems.

These companies collectively accounted for nearly 40% of Mexico’s total CABLE ELECTRICO imports, emphasizing a concentrated market structure dominated by multinational manufacturers.

Leading Suppliers to Mexico

On the export side, 383 suppliers provided electric cables to Mexico during the first half of 2025. The supply network reflects a strong presence of Asian and European firms, with China serving as the predominant source country. The key suppliers include:

STANDAR ELECTRIC WIRE & CABLE CO., LTD. – Mexico’s leading cable supplier, exporting USD 2.65 million worth of cables, mainly to IDL International.

FURUKAWA AUTOMOTIVE SYSTEMS INC. – A Japanese automotive cabling specialist, delivering high-precision wiring systems valued at USD 0.18 million.

KYUNGSHIN AMERICA CORP.– Exported USD 0.57 million, serving clients like KYUNGSHIN MEXICO OBREGON.

AMERICAN POWER CONVERSION CORPORATION (A.P.C.) B.V.– A key European exporter of industrial cables, supplying Schneider Electric’s Mexican division.

SHANDONG GROWTH YEAR SUPPLY CHAIN CO., LTD.– Provided USD 0.10 million worth of cables, further strengthening China’s footprint in Mexico’s import market.

After removing logistics and intermediary entities, these five suppliers represent Mexico’s most direct and active foreign partners in this HS category.

Trade Regions and Focus Markets

Regional trade patterns reveal that China overwhelmingly dominates Mexico’s CABLE ELECTRICO imports. From January to June 2025, Chinese exports totaled USD 32.29 million, representing over 75% of Mexico’s total import value. Secondary partners include South Korea (USD 2.97 million), the Philippines (USD 0.54 million), Germany (USD 0.43 million), and the Czech Republic (USD 0.65 million).

This regional composition underscores the globalized structure of the electric cable supply chain, where East Asian countries serve as key suppliers of both raw materials and finished harness systems. Europe’s participation—particularly from Germany and Hungary—tends to center around automotive-grade and industrial control wiring.

The dominant Chinese presence aligns with Mexico’s manufacturing strategy, which relies on imported electrical components for assembly and re-export through maquiladora operations. This integration of Asian supply chains supports both domestic and North American production bases.

Focus Country: China’s Influence

China remains Mexico’s foremost trade partner in the CABLE ELECTRICO category. The bilateral trade between these two economies demonstrates a robust exchange, supported by consistent supply volumes and competitive pricing. Chinese exporters such as STANDAR ELECTRIC WIRE & CABLE CO., LTD. and SUZHOU CABLEPLUS ELECTRIC CO., LTD. have established strong relationships with Mexico’s largest buyers, including IDL International and LGMG de México.

Sample import items from China include automotive wiring harnesses, multi-core power cables, and industrial signal cords—components essential for Mexico’s automotive and consumer electronics sectors. The reliability and cost-effectiveness of Chinese suppliers have made them indispensable to Mexico’s manufacturing ecosystem.

Market Trends and Analysis

The upward trajectory of Mexico’s CABLE ELECTRICO imports highlights several converging factors:

-

Automotive Expansion: Mexico continues to attract major automotive manufacturers, increasing demand for high-performance wiring systems and harnesses.

-

Renewable Energy Projects: The shift toward solar and wind energy has spurred imports of power cables designed for energy transmission infrastructure.

-

Nearshoring Dynamics: As global firms diversify supply chains closer to the U.S. market, imports of electronic and electrical components into Mexico are expected to remain strong.

-

Technological Diversification: New applications in smart homes, electric vehicles, and industrial automation are expanding cable specifications and boosting total import volumes.

From a trade perspective, the average import price per kilogram of electric cable from China is significantly lower than that of European suppliers, giving Asian manufacturers a competitive advantage. Nevertheless, European imports continue to command higher prices due to specialized engineering and compliance with industrial standards.

Summary and Outlook

Between January and June 2025, Mexico’s imports of electric cables (HS 85444299) demonstrated sustained growth, totaling USD 42.53 million in value and 2.83 million kilograms in weight. The market is heavily concentrated among a few major importers—led by Foxconn, Hisense, and Schneider Electric—and equally dependent on a limited number of East Asian suppliers.

As Mexico deepens its industrial integration with North America, the demand for imported electrical components is projected to remain robust. Future growth will likely be driven by investments in EV manufacturing, infrastructure modernization, and automation technologies, areas where high-quality cabling plays a crucial role.

Overall, the data affirms that electric cables remain a vital import segment within Mexico’s industrial landscape—reflecting not only domestic production demands but also the country’s position as a global manufacturing hub connecting Asia and the Americas.

Data Source

All data cited in this article are sourced from NBD DATA

For detailed insights or enterprise-level trade data services, please visit NBD DATA Service