Resilient Growth in India’s Rubber Seal Market: Analyzing O-Ring Imports and Global Supply Trends

From January to June 2025, India’s import market for O-Rings (HS Code 40169320

This continuous growth reflects India’s expanding industrial base and its deepening integration into global manufacturing supply chains. The trade involved 63 exporting countries, with 1,866 Indian importers and 2,846 foreign suppliers actively participating in the market.

Import Trends: Quantities and Trade Dynamics

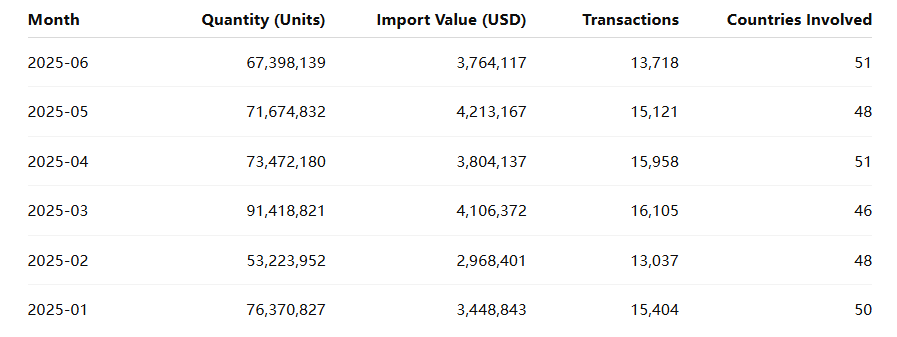

Between January and June 2025, India’s O-Ring imports maintained a consistent upward trajectory. The highest import values were recorded in May (USD 4.21 million) and March (USD 4.10 million), while the total import quantity exceeded 430 million units in just six months.

Import activity was stable throughout the half-year period. March recorded the largest quantity (91.4 million units), while May reached the highest total value, indicating demand for higher-specification O-Rings.

The rising import volume suggests growing use of imported seals in India’s automotive manufacturing, precision equipment, and engineering maintenance sectors.

Key Importers and Market Leaders

India’s O-Ring market is characterized by a mix of multinational subsidiaries and leading domestic industrial players. The top importers include:

1. GMORS India Pvt. Ltd.

As a subsidiary of Taiwan’s GE MAO RUBBER INDUSTRIAL CO., LTD., GMORS India led the O-Ring import segment with over 43 million units, totaling USD 729,948. Most imports came from Taiwan(China) and Thailand, supplied by GE MAO RUBBER INTERNATIONAL (Thailand) Co., Ltd. and Applied Seals Co., Ltd.. These O-Rings are used in automotive systems and industrial sealing applications requiring oil and heat resistance.

2. Trelleborg India Private Limited

Sweden’s Trelleborg Group, through its Indian subsidiary, imported approximately 15.5 million O-Rings valued at USD 800,000. Key suppliers included Trelleborg Sealing Solutions Germany GmbH and Trelleborg UK Ltd.. These products are used in high-performance sectors such as aerospace, medical devices, and precision machinery.

3. Komatsu India Private Limited

Komatsu India imported about 512,000 units worth USD 146,784, mainly from Japan’s Komatsu Ltd., Komatsu Logistics Corp., and Goh Shoji Co., Inc. The demand reflects India’s steady investment in construction and mining equipment production.

4. Tata Hitachi Construction Machinery Co. Pvt. Ltd.

Tata Hitachi imported around 389,000 units, valued at USD 122,318, from Hitachi Construction Machinery (Japan) and related subsidiaries. These O-Rings are primarily used in hydraulic systems and excavator assembly lines.

5. Horiba India Private Limited

Horiba India, a leading scientific equipment manufacturer, imported 9,211 units of precision sealing products worth USD 27,809 from Horiba Techno Service Co., Ltd. (Japan) and Horiba Instruments Inc. (U.S.). These are used in analytical and measuring instruments requiring airtight performance.

Major Global Suppliers

India’s O-Ring imports are supported by a wide network of global suppliers, particularly from Asia and Europe:

-

GE MAO RUBBER INDUSTRIAL CO., LTD.

– Taiwan(China) -

APPLIED SEALS CO., LTD.

– Taiwan(China) -

CATERPILLAR S.A.R.L. SINGAPORE

– Singapore -

ALFA LAVAL TECHNOLOGIES AB

– Sweden

These suppliers provide O-Rings for various applications — from heavy machinery and compressors to food and energy equipment — ensuring that India’s manufacturing ecosystem remains globally competitive.

Trade Regions and Global Integration

India’s O-Ring imports originated from 63 countries, demonstrating a high level of trade diversification.

The main sourcing regions were:

-

East Asia (Taiwan(China), Japan, China) – Automotive and industrial-grade O-Rings

-

Europe (Germany, Sweden, UK) – High-precision and aerospace sealing systems

-

ASEAN & South Korea – General-purpose rubber seals

-

North America (U.S., Canada) – Specialty elastomers and advanced sealing materials

This geographic distribution illustrates India’s dual strategy: sourcing high-quality O-Rings from developed markets while maintaining cost efficiency through Asian regional suppliers.

Market Insights and Industrial Implications

The O-Ring import pattern reflects India’s broader industrial transformation:

-

Industrial Modernization: The shift toward automation and precision machinery has boosted demand for high-performance sealing components.

-

OEM Integration: Companies such as Komatsu, Trelleborg, and GMORS integrate imported O-Rings directly into assembly lines, enhancing reliability and consistency.

-

Supply Chain Resilience: With nearly 3,000 exporters and 1,800 importers, India’s supply network remains diversified and competitive.

Additionally, the automotive and electronics industries are expected to further increase O-Ring demand, particularly for heat- and chemical-resistant materials.

Conclusion

India’s O-Ring imports in the first half of 2025 highlight its strong industrial momentum and integration within global manufacturing systems. Importing over 430 million units in just six months shows how critical these small components are to modern production.

From construction machinery and vehicles to analytical equipment and automation, O-Rings play an essential role in ensuring efficiency and reliability.

As analyzed by NBD DATA

Data Source

All trade data and analysis are based on India’s customs records for January–June 2025, processed by NBD DATA