Industrial Insight: Nigeria’s 2025 Import Trends in Molding Machinery Components

In the first half of 2025, Nigeria’s imports under HS Code 8477900000

According to data from NBD DATA

The imported products mainly consist of injection molding parts, mold bases, extrusion machine components, and auxiliary mechanical elements used in producing plastic containers, films, pipes, and rubber-based industrial goods. Such imports are vital for Nigeria’s industrial diversification agenda and are directly linked to the expansion of consumer goods and packaging industries.

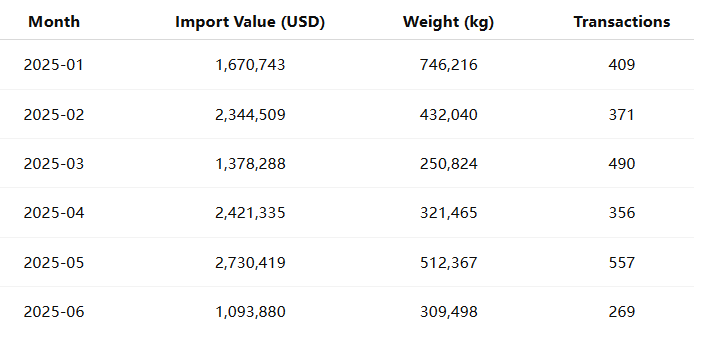

Monthly Trend Overview

Nigeria’s import performance for molding machinery components remained consistent but showed distinct momentum in the second quarter of 2025, reflecting renewed industrial procurement cycles.

The import volume peaked in May 2025, exceeding USD 2.73 million, suggesting intensified acquisition of spare parts and machinery accessories before mid-year production cycles. January and February also showed strong purchasing activity, possibly related to restocking plans following 2024’s supply chain constraints.

Overall, Nigeria’s H1 2025 data reveal an average monthly import value of USD 1.94 million, emphasizing the industrial sector’s reliance on imported machinery components for manufacturing continuity.

Market Observation: Leading Importers and Supply Networks

The market for molding machinery components in Nigeria is dominated by several established players that support the country’s growing manufacturing ecosystem.

Top importers include:

-

VIVA Metal & Plastic Industries Ltd. — a major participant in Nigeria’s plastic packaging segment, recorded imports worth USD 613 thousand, sourcing components primarily from SVANOSIO Company Limited and Lancer (Shanghai) Int’l Trading Co., Ltd.

-

Nigeria Pipes Ltd. Kano

— focusing on pipe and extrusion technologies, imported parts valued at USD 467 thousand, with key suppliers including Battenfeld Cincinnati Germany GmbH and Battenfeld Cincinnati Austria GmbH. -

Krones LCS Center West Africa Ltd. — a key service hub for bottling systems, imported USD 274 thousand worth of components from Krones AG, Neutraubling (Germany).

-

Pentagon Plastic Industries Ltd. — an established manufacturer of packaging products, accounted for USD 510 thousand in imports, collaborating with Husky Injection Molding Systems S.A. and Jon Wai Machinery Works Co., Ltd.

-

SACVIN Nigeria Ltd. — specializing in plastic and polymer production, reported imports worth USD 333 thousand, sourced from Vision Fuse FZCO and Kinara International Ltd.

-

Nigerian Bottling Company Ltd. — the bottling arm of Coca-Cola in Nigeria, registered USD 1.39 million in imports, with notable suppliers including Sidel Blowing & Services SAS and Husky Injection Molding Systems.

Collectively, these firms illustrate a diversified yet machinery-dependent ecosystem. Imports are primarily destined for packaging, beverage bottling, plastic extrusion, and footwear manufacturing facilities across Lagos, Kano, and Port Harcourt.

Regional Trade Insights

From a regional perspective, Nigeria’s supply network for molding machinery components in H1 2025 was dominated by Asia and Europe, with minor contributions from the Americas and Africa.

Asia, led by China, India, and the UAE, accounted for approximately 45% of total imports, supplying cost-efficient mold parts, extrusion elements, and auxiliary components.

Europe, especially Germany, Austria, and France, contributed about 40% of the value, providing precision-engineered components from brands like Krones AG, Battenfeld Cincinnati, and Sidel SAS.

The remaining 15% came from other regions — notably the USA, Turkey, and South Africa — representing regional engineering firms and specialized component exporters.

This pattern underscores Nigeria’s strategy of balancing affordability and technical performance in its industrial imports.

Industrial Dynamics and End-Use Sectors

The surge in imports under HS 8477900000 aligns with Nigeria’s ongoing efforts to expand domestic manufacturing capacity. The components are primarily utilized in:

-

Plastic packaging and bottling plants — supporting fast-moving consumer goods (FMCG) industries.

-

Automotive and construction sectors — through rubber molding parts and pipe extrusion lines.

-

Agro-processing and household goods manufacturing — involving blow-molding machines and injection molds.

The participation of companies like KRONES LCS Center West Africa and SACVIN Nigeria Ltd. underscores how international partnerships facilitate technology transfer and equipment maintenance within Nigeria’s industrial base.

The import growth also reflects capital investment in machinery maintenance, a crucial step for prolonging equipment life amid limited local production capabilities for specialized spare parts.

Focus on German and Chinese Machinery Partnerships

A distinctive feature of the Nigerian machinery components market is its dual dependency on both German precision equipment and Chinese cost-efficient manufacturing solutions.

German suppliers like Krones AG and Battenfeld Cincinnati serve high-end beverage and extrusion industries that demand durable and technologically advanced components.

Meanwhile, Chinese exporters — particularly Lancer (Shanghai) International Trading Co., Ltd. and Vision Fuse FZCO — provide large-volume, budget-friendly parts that meet the operational needs of mid-sized Nigerian manufacturers.

This balance allows Nigerian industries to maintain flexibility across different production scales, ensuring machinery uptime while controlling operational expenditure.

Summary

Between January and June 2025, Nigeria imported USD 11.64 million worth of molding machinery components (HS 8477900000), weighing 2.57 million kg across 2,452 transactions. The data underscore Nigeria’s growing industrial base, particularly in plastic, packaging, and beverage manufacturing.

Key industrial importers such as VIVA Metal & Plastic Industries Ltd.

With China and Germany leading as primary suppliers, Nigeria’s molding and manufacturing ecosystem benefits from a blend of affordability, precision, and continuous technology inflow.

Looking ahead, further growth is expected in H2 2025 as Nigerian industries pursue localized assembly of packaging equipment and expand polymer-based production capacity.

Data Source

All figures and company details are derived from the verified trade intelligence database of NBD DATA

For comprehensive industry insights or customized trade analytics, please visit https://en.nbd.ltd/service